Introduction

This article describes an example workflow for fitting and validating

metamodels, and making predictions using these metamodels, using the

pacheck package. The types of metamodel which the package

supports are: linear model, random forest model, and lasso model. All

three metamodels are covered. Note: This vignette is

still in development.

We will use the example dataframe df_pa which is included

in the package.

*** Note: the functions for fitting the linear model and the random forest model both include a ‘validation’ argument. So it is also possible to validate the model using those functions. However, there is also a separate function for the validation process available. ***

Model Fitting & Parameter Information

Functions: fit_lm_metamodel,

fit_rf_metamodel, fit_lasso_metamodel.

For all three models (linear model, random forest model, and lasso

model), there is a separate function used to fit the model.

The random seed number chosen for these examples is 24.

Linear Model

Arguments: df, y_var, x_vars,

seed_num.

We fit the linear model, and obtain the coefficients.

lm_fit <- fit_lm_metamodel(df = df_pa,

x_vars = c("rr",

"u_pfs",

"u_pd",

"c_pfs",

"c_pd",

"c_thx",

"p_pfspd",

"p_pfsd",

"p_pdd"),

y_var = "inc_qaly",

seed_num = 24,

show_intercept = TRUE)

lm_fit$fit##

## Call:

## lm(formula = form, data = df)

##

## Coefficients:

## (Intercept) rr u_pfs u_pd c_pfs c_pd

## 1.363e+00 -1.293e+00 6.275e-01 -3.539e-01 -7.602e-06 -4.512e-06

## c_thx p_pfspd p_pfsd p_pdd

## -1.349e-05 -2.850e-01 -3.632e+00 8.003e-01Variable Transformation

Arguments: standardise, x_poly_2,

x_poly_3, x_exp, x_log,

x_inter.

The function also allows for the transformation of input

variables.

In the following model we standardise the regression parameters by

setting the standardise argument to TRUE. Standardisation

is performed as follows:

where

is the value of parameter

,

the mean value of parameter

,

and

its standard deviation.

lm_fit <- fit_lm_metamodel(df = df_pa,

x_vars = c("rr",

"u_pfs",

"u_pd",

"c_pfs",

"c_pd",

"c_thx",

"p_pfspd",

"p_pfsd",

"p_pdd"),

y_var = "inc_qaly",

seed_num = 24,

standardise = TRUE

)

lm_fit$fit##

## Call:

## lm(formula = form, data = df)

##

## Coefficients:

## (Intercept) rr u_pfs u_pd c_pfs c_pd

## 0.270658 -0.085924 0.045913 -0.035886 -0.001470 -0.001818

## c_thx p_pfspd p_pfsd p_pdd

## -0.001336 -0.010220 -0.106710 0.032889Here we transform several variables: rr will be

exponentiated by factor 2, c_pfs & c_pd by

factor 3, we take the exponential of u_pfs &

u_pd, and the logarithm of p_pfsd.

lm_fit <- fit_lm_metamodel(df = df_pa,

x_vars = c("p_pfspd",

"p_pdd"),

x_poly_2 = "rr",

x_poly_3 = c("c_pfs","c_pd"),

x_exp = c("u_pfs","u_pd"),

x_log = "p_pfsd",

y_var = "inc_qaly",

seed_num = 24

)

lm_fit$fit##

## Call:

## lm(formula = form, data = df)

##

## Coefficients:

## (Intercept) p_pfspd p_pdd poly(rr, 2)1

## -0.97789 -0.31460 0.81577 -2.70951

## poly(rr, 2)2 poly(c_pfs, 3)1 poly(c_pfs, 3)2 poly(c_pfs, 3)3

## 0.41879 -0.03477 -0.07427 0.01652

## poly(c_pd, 3)1 poly(c_pd, 3)2 poly(c_pd, 3)3 exp(u_pfs)

## -0.02696 0.02767 0.03326 0.29926

## exp(u_pd) log(p_pfsd)

## -0.19412 -0.35528And lastly, we can also include an interaction term between

p_pfspd and p_pdd.

lm_fit <- fit_lm_metamodel(df = df_pa,

x_vars = c("p_pfspd",

"p_pdd"),

x_poly_2 = "rr",

x_poly_3 = c("c_pfs","c_pd"),

x_exp = c("u_pfs","u_pd"),

x_log = "p_pfsd",

x_inter = c("p_pfspd","p_pdd"),

y_var = "inc_qaly",

seed_num = 24

)

lm_fit$fit##

## Call:

## lm(formula = form, data = df)

##

## Coefficients:

## (Intercept) p_pfspd p_pdd poly(rr, 2)1

## -0.93155 -0.61761 0.59049 -2.70483

## poly(rr, 2)2 poly(c_pfs, 3)1 poly(c_pfs, 3)2 poly(c_pfs, 3)3

## 0.41959 -0.03496 -0.07264 0.01523

## poly(c_pd, 3)1 poly(c_pd, 3)2 poly(c_pd, 3)3 exp(u_pfs)

## -0.02689 0.02731 0.03460 0.29812

## exp(u_pd) log(p_pfsd) p_pfspd:p_pdd

## -0.19352 -0.35546 1.50843Random Forest Model

The random forest metamodel are fitted using the randomForestSRC

R package. Arguments: df, y_var,

x_vars, seed_num.

Note that for the RF model several variables are omitted to reduce computation time

rf_fit <- fit_rf_metamodel(df = df_pa,

x_vars = c("rr",

"u_pfs",

"u_pd"),

#"c_pfs",

#"c_pd",

#"c_thx",

#"p_pfspd",

#"p_pfsd",

#"p_pdd"),

y_var = "inc_qaly",

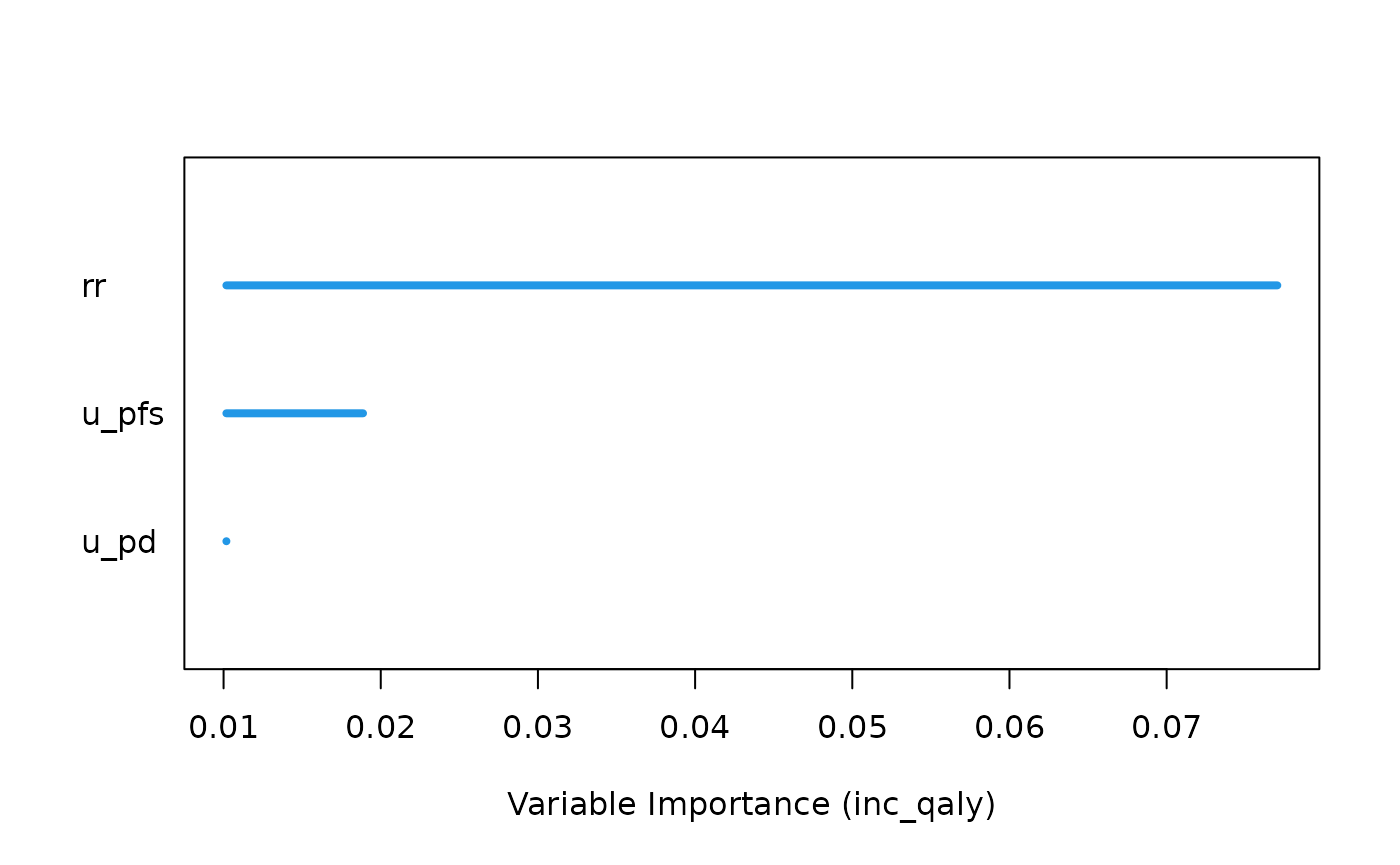

seed_num = 24)Variable importance

Setting the var_importance argument to TRUE returns a

plot which shows the importance of the included x-variables. The larger

the number is, the more important the variable is, meaning that it

greatly reduces the out-of-bag (OOB) error rate compared to the other

x-variables.

rf_fit <- fit_rf_metamodel(df = df_pa,

x_vars = c("rr",

"u_pfs",

"u_pd"),

#"c_pfs",

#"c_pd",

#"c_thx",

#"p_pfspd",

#"p_pfsd",

#"p_pdd"),

y_var = "inc_qaly",

var_importance = TRUE,

seed_num = 24)

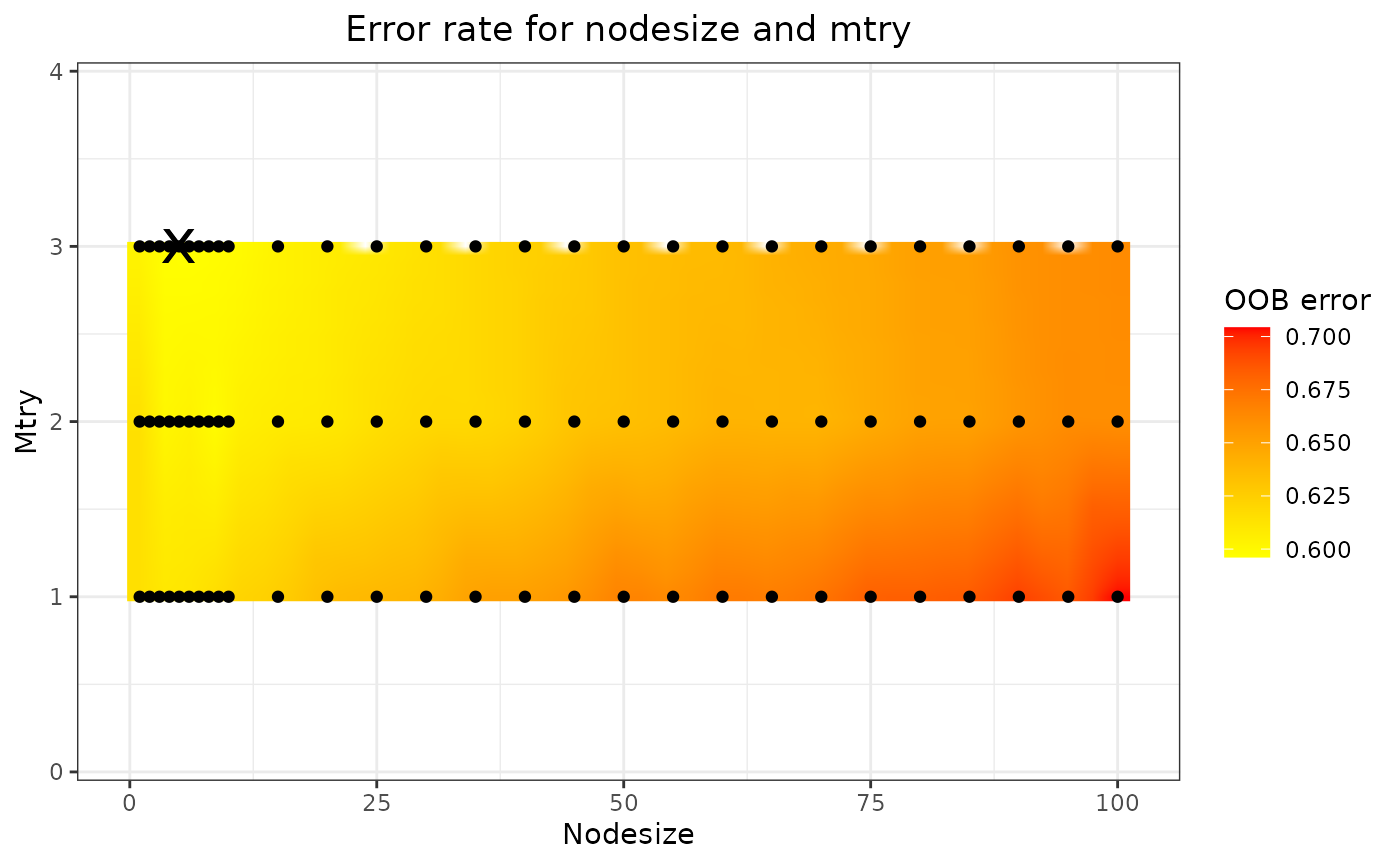

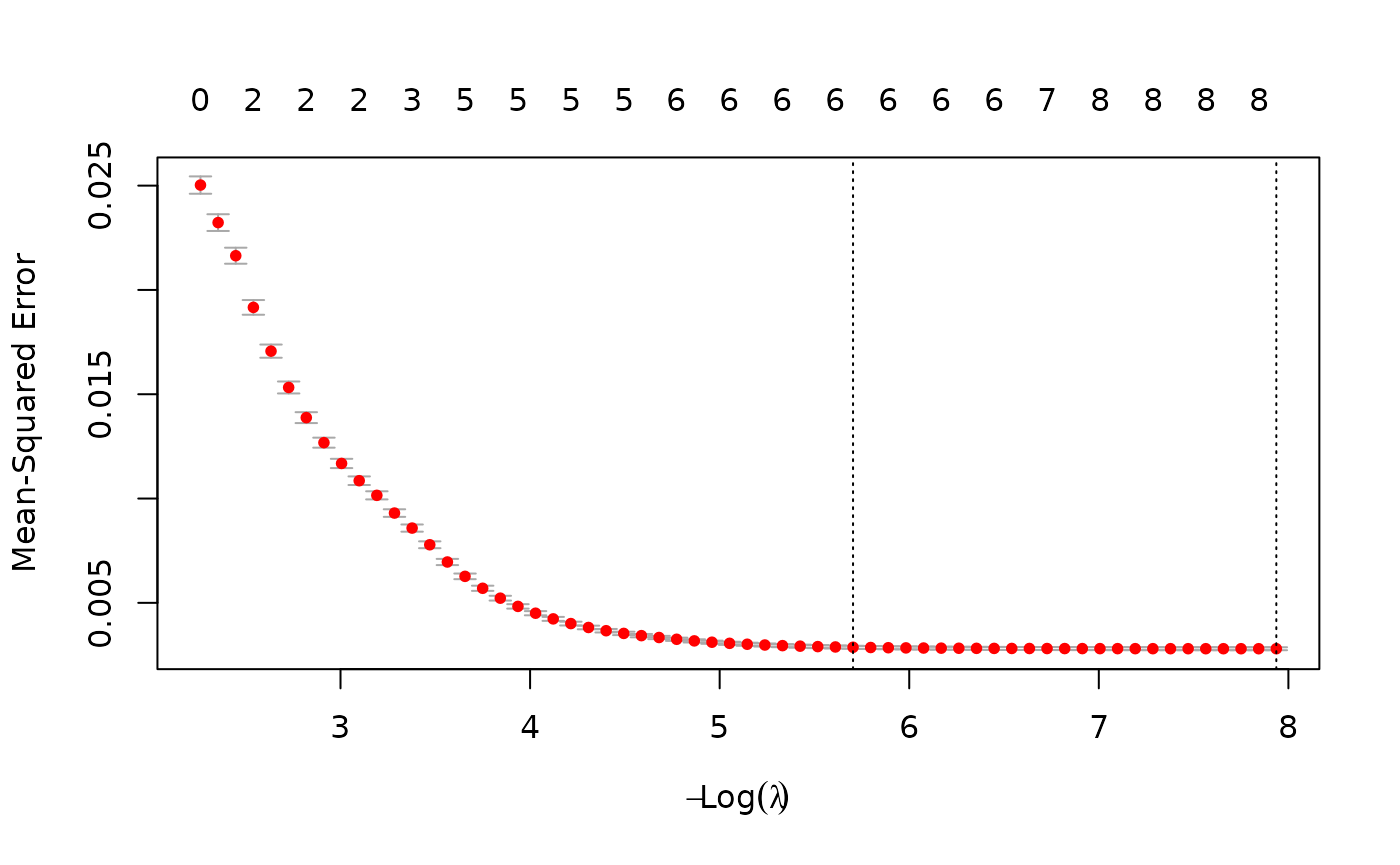

Tuning nodesize and mtry

By using the tune argument , two parameters which can

have a significant impact on the model fit are nodesize

(the minimal size of the terminal node) and mtry (the

number of variables to possibly split at each node) are optimised to

improve model fit. The tuning process consists of a grid search. If

tune = FALSE, default values for nodesize and

mtry are used, which are 5 and (nr of x-variables)/3,

respectively.

rf_fit <- fit_rf_metamodel(df = df_pa,

x_vars = c("rr",

"u_pfs",

"u_pd"),

#"c_pfs",

#"c_pd",

#"c_thx",

#"p_pfspd",

#"p_pfsd",

#"p_pdd"),

y_var = "inc_qaly",

var_importance = FALSE,

tune = TRUE,

seed_num = 24)

rf_fit$tune_fit$optimal## nodesize mtry

## 1 3

rf_fit$tune_plot

The optimal nodesize and mtry can be found

in the rf_fit$tune_fit$optimal element of the list, and the

results are shown in the plot (in this case

rf_fit$tune_plot). On this plot, the black dots represent

the combinations of nodesize and mtry that

have been tried, the colour gradient is obtained through 2-dimensional

interpolation. The black cross marks the optimal combination, i.e., the

combination yielding the lowest OOB error.

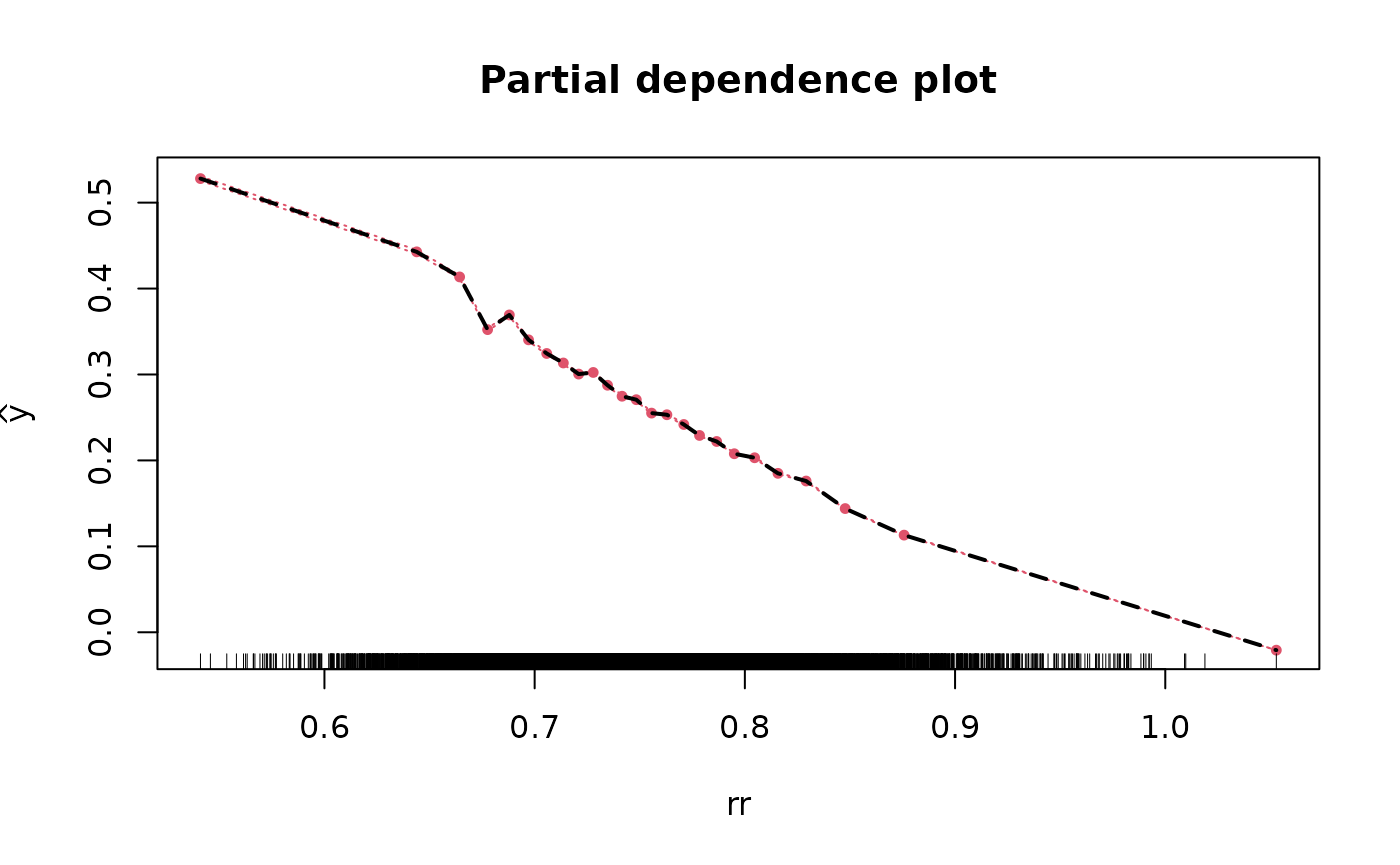

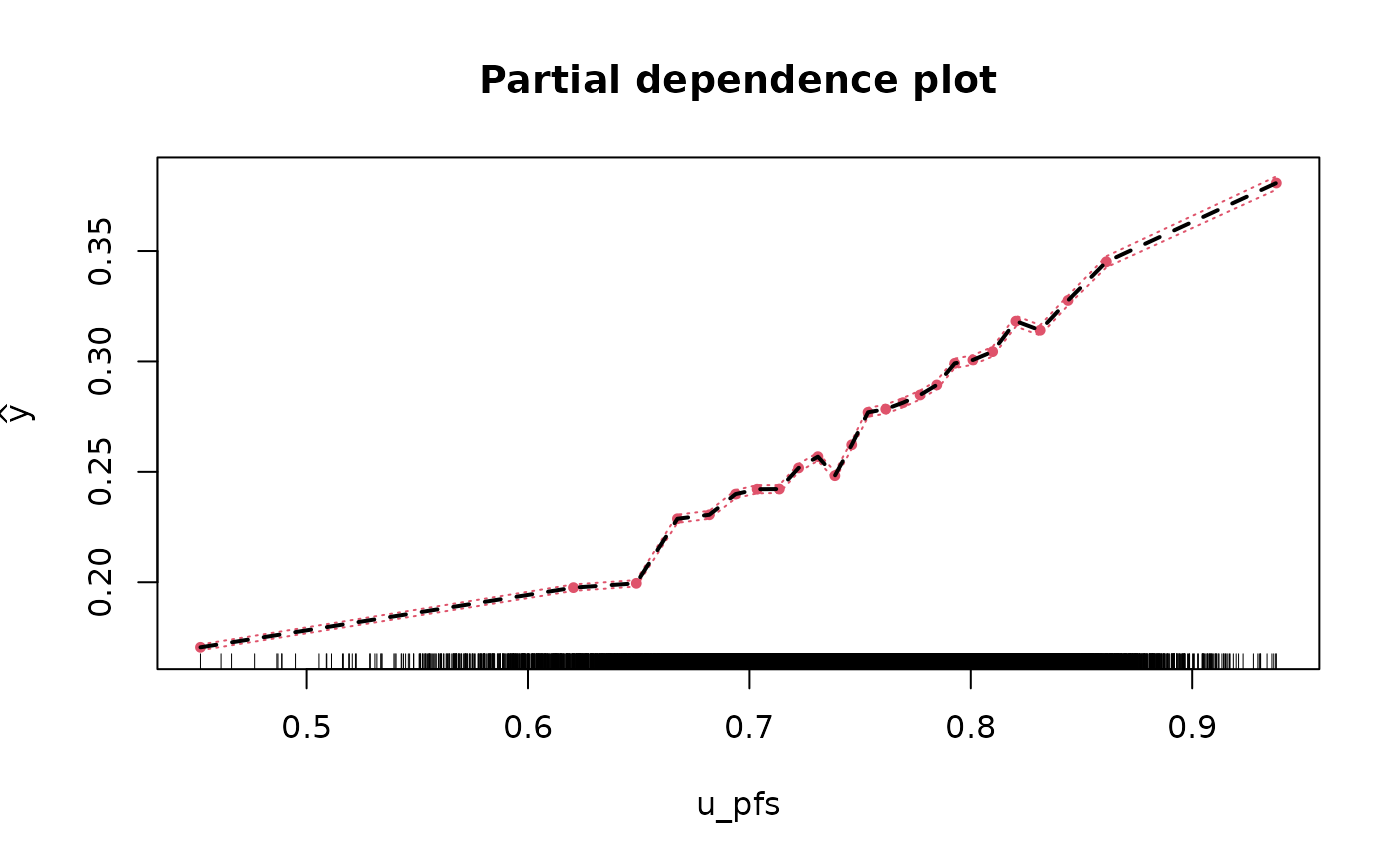

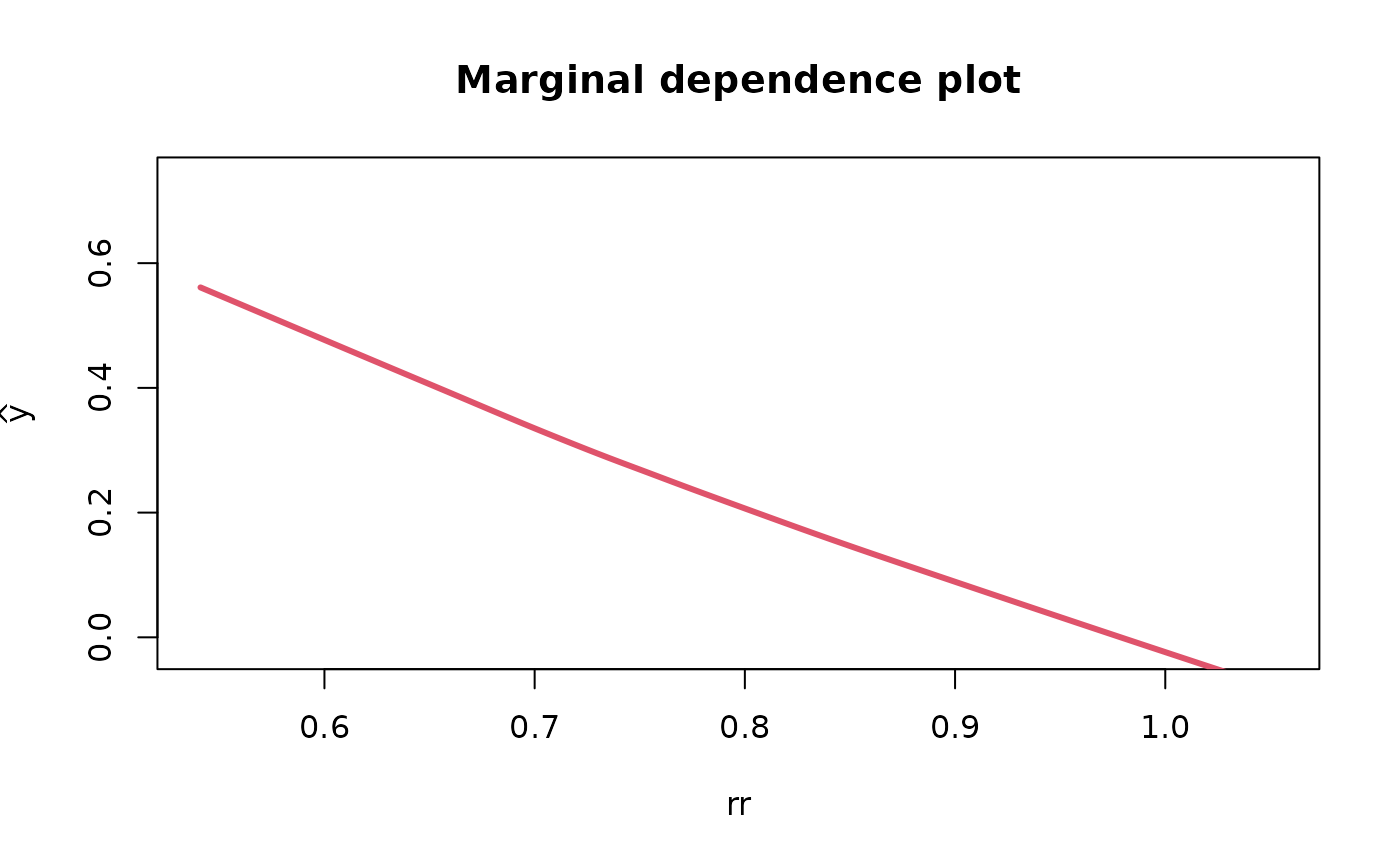

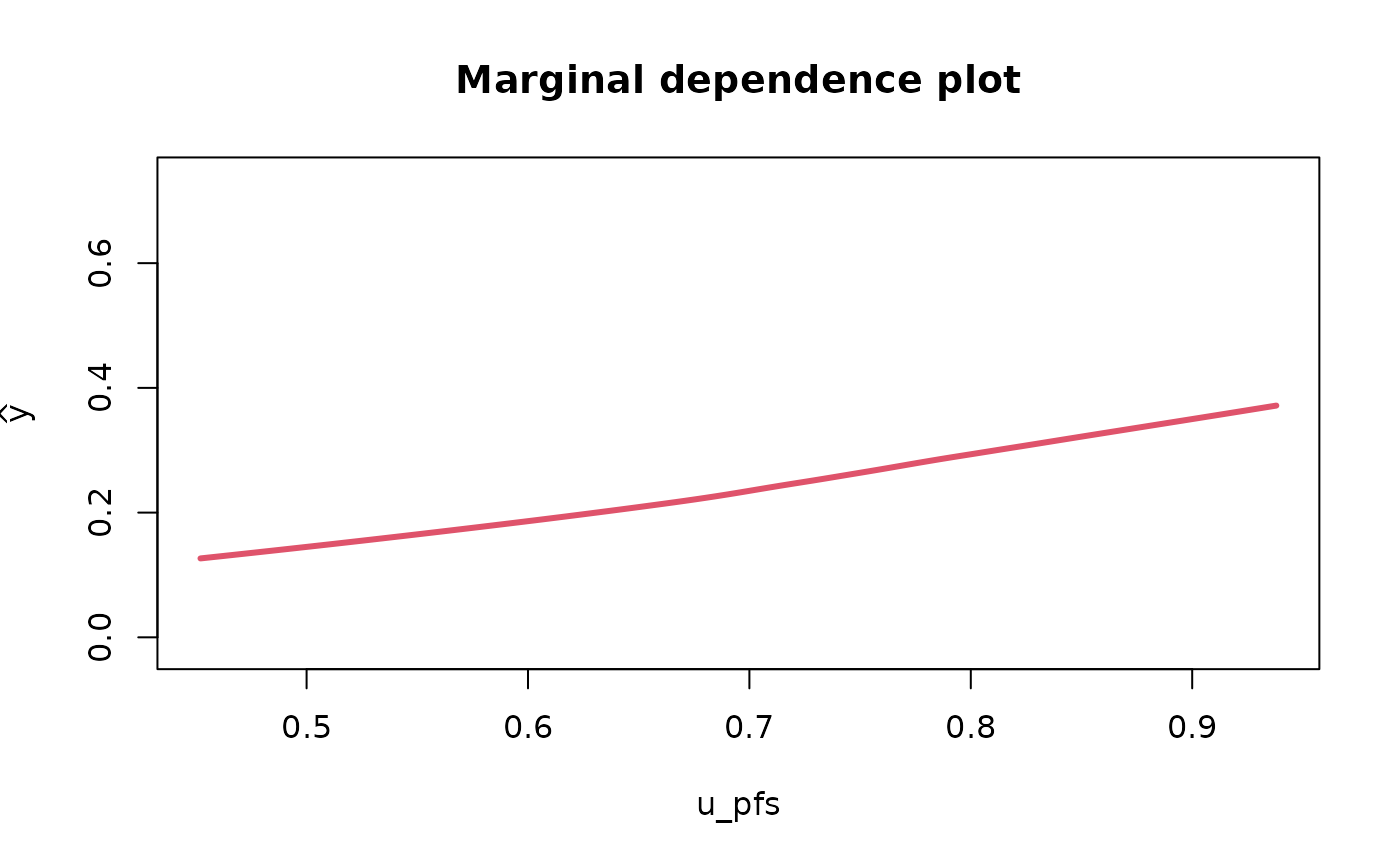

Partial & marginal plots

We can obtain partial and marginal plots, by setting

pm_plot equal to ‘partial’, ‘marginal’, or ‘both’.

pm_vars specifies for which variables the plot must be

constructed.

rf_fit <- fit_rf_metamodel(df = df_pa,

x_vars = c("rr",

"u_pfs",

"u_pd"),

#"c_pfs",

#"c_pd",

#"c_thx",

#"p_pfspd",

#"p_pfsd",

#"p_pdd"),

y_var = "inc_qaly",

var_importance = FALSE,

tune = TRUE,

pm_plot = "both",

pm_vars = c("rr","u_pfs"),

seed_num = 24)

Lasso Model

We fit the lasso model and obtain the coefficients using all parameter values from all iterations.

lasso_fit <- fit_lasso_metamodel(df = df_pa,

x_vars = c("rr",

"u_pfs",

"u_pd",

"c_pfs",

"c_pd",

"c_thx",

"p_pfspd",

"p_pfsd",

"p_pdd"),

y_var = "inc_qaly",

tune_plot = TRUE,

seed_num = 24)

lm_fit$fit##

## Call:

## lm(formula = form, data = df)

##

## Coefficients:

## (Intercept) p_pfspd p_pdd poly(rr, 2)1

## -0.93155 -0.61761 0.59049 -2.70483

## poly(rr, 2)2 poly(c_pfs, 3)1 poly(c_pfs, 3)2 poly(c_pfs, 3)3

## 0.41959 -0.03496 -0.07264 0.01523

## poly(c_pd, 3)1 poly(c_pd, 3)2 poly(c_pd, 3)3 exp(u_pfs)

## -0.02689 0.02731 0.03460 0.29812

## exp(u_pd) log(p_pfsd) p_pfspd:p_pdd

## -0.19352 -0.35546 1.50843The plot shows the tuning results: the error rate for each lambda. The smallest lambda is chosen for the full model.

Generally, the lasso procedure yields sparse models, i.e., models that involve only a subset of the set of input variables. In this case however, no coefficients are set to 0, and we have the same results as we obtained from the linear model.

Model Validation

Validating the metamodels can be performed using the

validation arguments of the metamodel functions, or by

using the validate_metamodel function.

Through the validate_metamodel function, three types of

validation methods can be used: the train/test split, (K-fold)

cross-validation, and using a new dataset. We will discuss each

validation method.

Train/test split and Linear Model

Arguments: method, partition.

First we use the train/test split. For this we need to specify

partition, which sets the proportion of the data that will

be used for the training data. We also set show_intercept

to TRUE for the calibration plot.

lm_validation = validate_metamodel(lm_fit,

method = "train_test_split",

partition = 0.8,

show_intercept = TRUE,

seed_num = 24)

lm_validation$stats_validation## Statistics Value (method: train/test split)

## 1 R-squared 0.914

## 2 Mean absolute error 0.032

## 3 Mean relative error 0.758

## 4 Mean squared error 0.002

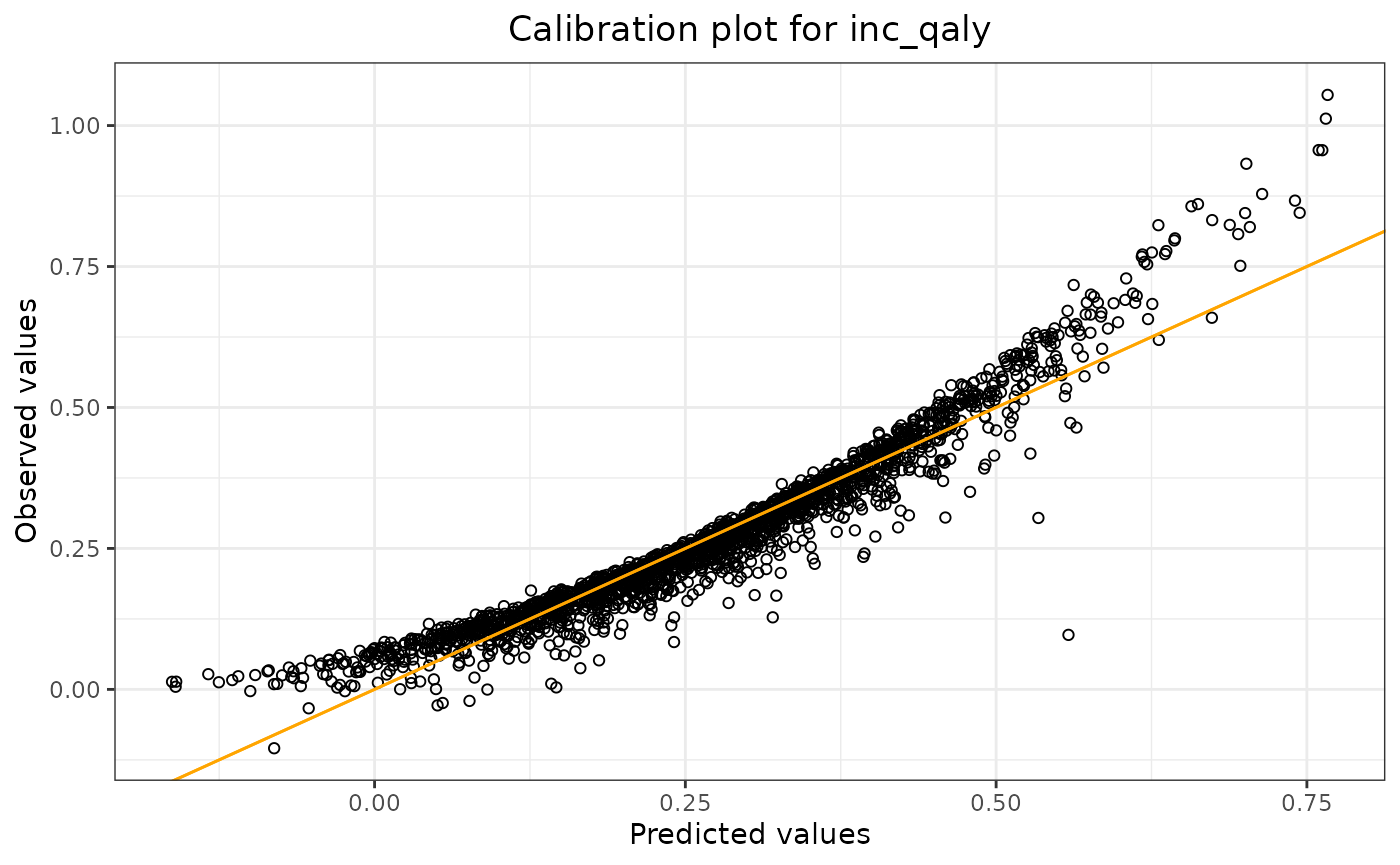

lm_validation$calibration_plot

The output shows the validation results: R-squared, mean absolute

error, mean relative error, and the mean squared error of the model

applied to the test data. By using

lm_validation$calibration_plot, we can display the

calibration plot.

K-fold Cross-Validation and Random Forest Model

Arguments: method, folds.

To use k-fold cross-validation, one needs to specify

method = "cross_validation". In the example, two folds are

used by specifying fold = 2.

rf_validation = validate_metamodel(rf_fit,

method = "cross_validation",

folds = 2,

seed_num = 24)

rf_validation$stats_validation## Statistic Value (method: cross-validation)

## 1 R-squared 0.343

## 2 Mean absolute error 0.098

## 3 Mean relative error 2.272

## 4 Mean squared error 0.017New Dataset and Lasso Model

Arguments: method, df_validate.

It also might happen that a validation dataset is obtained once the model has already been fitted some time ago. The function enables us to use this dataset for the validation process.

Since we only have one dataset, we first construct two datasets, where one dataset is used to fit the model, and the other is used to validate the model. Note that doing it like this, it is very similar to the train/test split method.

indices = sample(8000)

df_original = df_pa[indices,]

df_new = df_pa[-indices,]

lasso_fit2 <- fit_lasso_metamodel(df = df_original,

x_vars = c("rr",

"u_pfs",

"u_pd",

"c_pfs",

"c_pd",

"c_thx",

"p_pfspd",

"p_pfsd",

"p_pdd"),

y_var = "inc_qaly",

tune_plot = FALSE,

seed_num = 24)

lasso_validation <- validate_metamodel(lasso_fit2,

method = "new_test_set",

df_validate = df_new,

seed_num = 24)

rf_validation$stats_validation## Statistic Value (method: cross-validation)

## 1 R-squared 0.343

## 2 Mean absolute error 0.098

## 3 Mean relative error 2.272

## 4 Mean squared error 0.017Making Predictions

Function: predict_metamodel. Arguments:

inputs, output_type

There is one function which can be used to make predictions using the

fitted metamodels: predict_metamodel.

As an example, we will fit a four-variable model for all three metamodel types and with the following inputs:

| p_pfspd | p_pfsd | p_pdd | rr |

|---|---|---|---|

| 0.1 | 0.08 | 0.06 | 0.10 |

| 0.2 | 0.15 | 0.25 | 0.23 |

Thus we will obtain two predictions.

There are two ways to enter the inputs for the metamodel: as a vector or as a dataframe. The same holds for the output of the function: a vector or a dataframe. We will cover all four scenarios.

First we fit the models and define the inputs. Note that we do not validate the model first (which is not according to best practices) and use all available data to fit the models.

#fit the models

lm_fit2 = fit_lm_metamodel(df = df_pa,

x_vars = c("p_pfspd",

"p_pfsd",

"p_pdd",

"rr"),

y_var = "inc_qaly",

seed_num = 24)

rf_fit2 = fit_rf_metamodel(df = df_pa,

x_vars = c("p_pfspd",

"p_pfsd",

"p_pdd",

"rr"),

y_var = "inc_qaly",

tune = TRUE,

seed_num = 24

)

lasso_fit3 <- fit_lasso_metamodel(df = df_pa,

x_vars = c("p_pfspd",

"p_pfsd",

"p_pdd",

"rr"),

y_var = "inc_qaly",

tune_plot = FALSE,

seed_num = 24)

#define the inputs

ins_vec = c(0.1,0.2,0.08,0.15,0.06,0.25,0.1,0.23) #vector

ins_df = newdata #dataframe (defined above)Note that the order of the input vector matters. If we have a

four-variable model, and we want to make two predictions, the first two

values are for the first variable, the next two values are for the

second variable, etc. ‘First’ and ‘second’ refer to the placement of the

variable in the model as defined in the R-code. So in our example, the

first and second variable is p_pfspd and

p_pfsd, respectively.

1. Input: vector (Linear Model)

predictions = predict_metamodel(lm_fit2,

inputs = ins_vec,

output_type = "vector")

print(predictions)## [1] 1.0566582 0.75339562. Input: dataframe (Lasso Model)

predictions = predict_metamodel(lasso_fit3,

inputs = ins_df,

output_type = "vector")

print(predictions)## [1] 1.0528023 0.75103563. Output: vector (Random Forest Model)

predictions = predict_metamodel(rf_fit2,

inputs = ins_vec,

output_type = "vector")

print(predictions)## [1] 0.5019730 0.19205594. Output: dataframe (Linear Model)

predictions = predict_metamodel(lm_fit2,

inputs = ins_vec,

output_type = "dataframe")

print(predictions)## p_pfspd p_pfsd p_pdd rr predictions

## 1 0.1 0.08 0.06 0.10 1.0566582

## 2 0.2 0.15 0.25 0.23 0.7533956